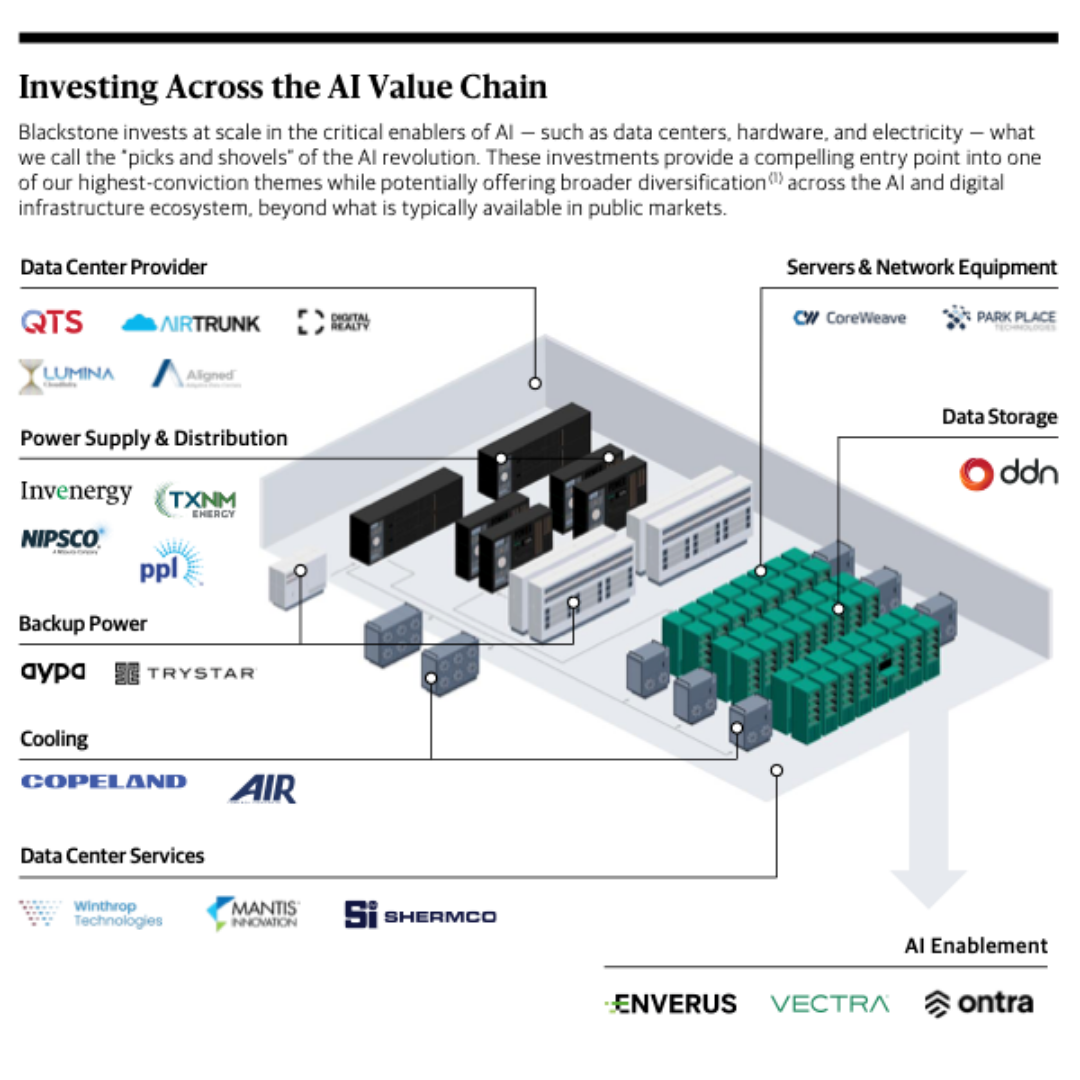

Article examines how the real beneficiaries of the AI revolution may not be software companies but the builders of its underlying infrastructure — from semiconductors and data centers to power and connectivity. The paper highlights how AI’s rapid expansion is driving a new, capital-intensive investment cycle anchored in physical assets. For investors, it underscores that the most durable long-term value may lie in the “picks and shovels” fueling the intelligence economy.

Article examines how the real beneficiaries of the AI revolution may not be software companies but the builders of its underlying infrastructure — from semiconductors and data centers to power and connectivity. The paper highlights how AI’s rapid expansion is driving a new, capital-intensive investment cycle anchored in physical assets. For investors, it underscores that the most durable long-term value may lie in the “picks and shovels” fueling the intelligence economy.

Read Full Article

Read Full Article